Small Business Restructure SBR: Save Your Business

Cash is tight. The ATO wants action, suppliers are shortening terms, and payroll lands before the next customer payment. In that position, directors do not need theory. You need a legal option that can keep the company trading while you deal with the debt pressure before it spills into personal risk.

A Small Business Restructure ("SBR") can do that. It gives an eligible company a formal process to put a compromise to creditors while directors stay in control of day-to-day trading. For a viable business, that is a serious advantage. You keep the operational wheel, the doors stay open, and the outcome is driven by a plan rather than a forced break-up.

Market results have given directors a reason to take the process seriously. Earlier reporting on ASIC-reviewed outcomes showed strong uptake, high creditor acceptance, and costs that often compare favourably with more traditional insolvency appointments. That matters, but the headline numbers only tell part of the story.

What generic guides miss is where restructures fail.

I have seen good businesses lose the SBR option because records were not current, employee entitlements were behind, tax lodgements had been ignored, or the proposal was thrown together too late. Once pressure builds, mistakes get expensive fast. A restructure practitioner can only work with the facts in front of them, and weak preparation can leave you exposed to a rejected plan, a failed appointment, or a much harsher liquidation path.

That is why the issue is not whether SBR exists. The issue is whether your company is ready for it, and whether the advice you get is director-focused from the start. At LemonAide, we treat SBR as a strategy to protect the business and reduce spillover risk to you personally, not as a box-ticking exercise. Done properly, it buys time, preserves control, and gives creditors a deal they may accept. Done poorly, it burns cash and closes off better options.

Introduction A Lifeline for Directors in Financial Distress

It often starts with a cash flow call you cannot avoid. The ATO is chasing arrears. A supplier wants payment before the next delivery leaves the warehouse. You are still trading, still invoicing, and still backing the business, but the pressure is no longer temporary.

This is the point where directors make expensive mistakes. Some wait for one good month to solve a structural debt problem. Others stop asking hard questions because the answers may force action. Delay does not protect you. It reduces room to act, weakens your position, and can increase the risk to you personally if the company keeps sliding.

A SBR gives an eligible company a formal way to put a deal to creditors while the directors keep control of day-to-day trading. It has been available in Australia since 1 January 2021. For the right business, it can preserve operations, protect value, and avoid the blunt force of a liquidation process started too late.

As noted earlier, market use of the process has shown that creditors will consider these proposals when the business is viable and the plan is credible. That matters, but directors should not read that as a guarantee. It is a legal process with strict entry conditions, disclosure obligations, and timing pressure.

Why directors are paying attention

Directors pay attention to SBR for one simple reason. It gives a company with a workable core business a chance to deal with debt without handing over the business at the outset.

That trade-off is commercially attractive, but it comes with a burden that generic guides often gloss over. You need current books, up-to-date lodgements, no outstanding employee entitlements especially surrounding superannuation, and a proposal that matches what the business can produce. If those basics are missing, the process can fail before creditors even get to the substance.

I have seen viable companies miss the window because they treated restructuring as paperwork instead of strategy. By the time they sought advice, cash had drained, records were unreliable, and the director had already made decisions that narrowed the available options.

The practical rule is simple. Test SBR early, before pressure strips away your choices.

At LemonAide, we approach SBR as a director protection strategy as much as a business recovery process. That means asking the uncomfortable questions early, stress-testing eligibility, and dealing with the compliance issues that can derail an appointment. Done properly, SBR can buy time and hold the business together. Done poorly, it wastes cash and can leave you facing a harsher outcome with fewer defences.

What Exactly Is a Small Business Restructure

A small business restructure is best understood as a controlled financial reset for an eligible company. It is not liquidation dressed up with nicer language. It is a formal process under insolvency law that allows a company to propose a compromise to creditors while continuing to trade under director control.

In a liquidation, the focus turns to winding up the company and dealing with its assets and liabilities after the point of failure. In an SBR, the focus is different. The question is whether the business can keep operating if its historic debt is reworked into something achievable.

The director in possession difference

The feature directors care about most is the director-in-possession model. In plain English, that means you stay in control of the company while the restructure is underway. You don’t get removed from day-to-day management at the start.

That changes the emotional temperature immediately. You can keep dealing with staff, customers, suppliers, and projects while the formal process runs. You’re not standing on the sidelines watching someone else make every operational decision.

The legal framework matters here too. The SBR process is governed by Part 5.3B of the Corporations Act 2001. It’s a real insolvency pathway, but one designed to preserve viable small businesses rather than rush them into shutdown.

What the practitioner actually does

An SBR still involves a registered liquidator. A Small Business Restructuring Practitioner works with the company to assess eligibility, review the company’s position, and propose a formulated proposal of the Director that goes to creditors. That practitioner is not there to run your business for you. Their role is supervisory and procedural, with a focus on whether the company can properly enter the process and whether the proposed plan is supportable.

A short explainer helps if you want to see the mechanics at a high level.

What SBR is good for and what it is not

SBR is well suited to companies that are under pressure but still have a functioning business underneath the debt. Typical examples include businesses with strong revenue but poor historical tax management, margin compression, a bad expansion decision, or a short-term cash flow shock that became chronic.

It is not a cure for every problem.

If the business is not viable, restructuring debt won’t fix the core issue.

If records are poor, the process becomes harder, slower, and riskier.

If directors hide transactions or liabilities, the proposal can unravel fast.

If directors have received a lockdown Director Penalty Notice or the non-lockdown Director Penalty Notice has expired, the proposal will not help you.

That’s why experienced advice matters. The legal process is only one layer. The core work is matching the process to a business that can survive after the debt is reprofiled.

Are You Eligible for the SBR Pathway

A director usually finds out very quickly whether SBR is a realistic option or a distraction. The pressure is already on. The ATO is chasing, suppliers are tightening terms, and cash flow is being used to plug old holes. If the company cannot clear the entry rules early, time is better spent choosing a different path before someone else forces it on you.

Directors should check four issues before spending money on a formal appointment:

Debt cap: Do the company’s total liabilities fall within the $1 million limit, excluding employee entitlements that are not due and payable?

Employee Entitlements: Does the company have outstanding employee entitlements that are due and payable, such as last quarters or last year's superannuation or annual leave of an employee that left last month?

Prior use: Has the company, or a related entity caught by the rules, already gone through SBR or simplified liquidation in the last seven years?

Company structure: Is the business trading through an eligible company, rather than a sole trader or partnership?

Records and disclosure: Can you produce financials, tax records, and a clear explanation of the company’s position without guesswork?

Fail the debt cap or the employee entitlements test and SBR is automatically off the table.

Struggle with structure, records, or disclosure and the position becomes more nuanced. Legal eligibility may still be there, but practical eligibility starts to fall apart. I have seen directors assume they were ready because the debt number worked, then lose momentum because no one could reconcile liabilities, explain related-party payments, or prove employee obligations were under paid.

Readiness decides whether eligibility is useful

The better question is not whether you are technically eligible on paper today. The better question is whether the company is ready to survive the scrutiny that comes with the process.

That is the part generic guides gloss over.

A company can sit just under the debt cap and still be in poor shape for SBR. Lodgements may be overdue. Creditor balances may be wrong. Director loan accounts may be messy. Old payment arrangements may have collapsed without being properly recorded. None of those issues automatically kill the process, but they create friction, cost, delay, and risk. They also increase the chance that a creditor, or the practitioner, takes a harder look at trading conduct before the appointment.

A rushed SBR exposes weak records, unresolved compliance failures, and wishful forecasting very quickly.

What directors should review before going further

| Issue | What directors should check |

|---|---|

| Liability position | Total company debts, including tax, trade creditors, loans, and contingent exposures |

| Employee obligations | Whether wages, leave, and super issues are current or likely to block progress |

| Tax compliance | Whether lodgements and records are current enough to support the process |

| Related party dealings | Whether past transactions will attract scrutiny or need explanation |

| Ongoing viability | Whether the company can trade profitably after debt relief |

Directors, therefore, need disciplined advice, not optimism. We are not trying to make an ineligible company look eligible. We are trying to identify what can be fixed lawfully, what needs to be disclosed properly, and whether the business is worth protecting at all. That is the difference between using SBR as a director-first protection strategy and stumbling into a process that leaves your personal risk exposed.

At LemonAide, we treat this stage as triage. We test the numbers, pressure-test compliance, and call out the weak spots before they become expensive surprises. If SBR fits, we help you enter it in a controlled way. If it does not, we say so early and protect your room to act.

The SBR Process Step by Step Through a Director's Eyes

Monday starts with a supplier threatening to stop stock supply. By Tuesday, the ATO is chasing arrears again. By Wednesday, you are asking the question directors usually leave too late. Can this company be saved without handing over control or risking a worse outcome later?

That is what the SBR process feels like from the director's chair. You are still running payroll, dealing with staff, calming key creditors, and trying to protect cash. At the same time, every assumption is being tested. The process is legal, structured, and time-limited, but the pressure on management is commercial and immediate.

Directors often hear that SBR lets them stay in control. That is true, but only part of the story. You keep control while carrying a heavy compliance burden. If records are poor, cash flow is unstable, or old transactions cannot be explained, that burden lands on you fast.

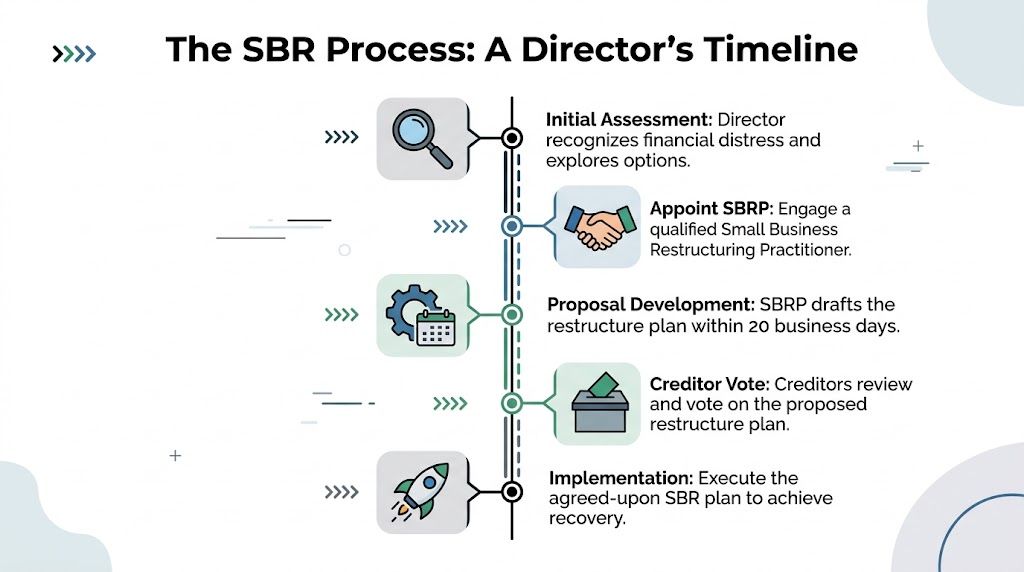

Stage one. The decision point

The process usually starts after informal fixes have failed. Payment plans are breaking. Creditors are losing patience. Debt has stopped being a cash-flow issue and become a solvency issue.

At that point, the question is not whether the business is under pressure. You already know that. The question is whether the underlying operation can produce profit if legacy unsecured debt is dealt with. If the answer is no, SBR can waste time you may not have. If the answer is yes, the formal appointment of a Small Business Restructuring Practitioner may be the right next move.

This decision is strategic. Enter too early, and you may spend money on a process the business did not need. Enter too late, and you increase the risk of failed implementation, creditor hostility, and scrutiny of your trading conduct before appointment.

Stage two. The 20 business day build

Once the practitioner is appointed, the proposal period begins. Directors stay in control of day-to-day trading while the restructuring plan is prepared over 20 business days, as noted earlier.

On paper, that window looks workable. In practice, it is tight. You need clean financial information, a clear debt position, supportable trading forecasts, and a proposal creditors can accept as realistic. At the same time, the business still has to trade properly. Staff still need answers. Customers still expect delivery.

The directors who struggle here are usually not careless. They are overloaded. They assume the books are close enough, the tax position can be cleaned up later, or the plan can be built around optimistic sales. Creditors and practitioners test those assumptions quickly.

A workable proposal usually rests on four things:

Books that match reality. Accounting files, bank statements, aged creditors, debtors, and ATO data need to line up.

Forecasts that can survive scrutiny. If projected revenue depends on a sudden jump in performance, the weakness will be obvious.

Explanations for unusual transactions. Related party payments, asset transfers, and selective creditor payments need a clear story and proper records.

Tight management during the build period. Random spending, new liabilities, and inconsistent communication can damage the plan before creditors even see it.

Stage three. The compliance pressure generic guides miss

This is the part many articles gloss over. SBR is simpler than larger formal insolvency processes, but it is not light-touch for directors.

Employee entitlements that are due and payable must be paid before the plan can go to creditors, as explained in Access Intell’s creditor guide to SBR. For some companies, that requirement is the hardest obstacle in the whole process. A business may be viable after debt compromise and still struggle to fund those payments at the point they are required.

There is more. The practitioner needs reliable information. Directors must make formal declarations. Historic conduct may need review. If tax lodgements are missing, records are incomplete, or liabilities have been understated, the issue is no longer administrative. It can derail the plan or expose the director position more broadly.

This is also where personal asset protection becomes practical, not theoretical. Sloppy preparation can lead to questions about solvency, director conduct, and what was known before the appointment. Good advice at this point is not about selling SBR. It is about reducing avoidable risk while preserving the option if the company qualifies.

Stage four. Creditor voting

Once the plan is finalised, creditors move into the voting period. They are not judging your effort. They are judging return and credibility.

A poor proposal usually fails for predictable reasons. The numbers do not reconcile. The forecast looks inflated. Related party dealings are not explained properly. The business asks creditors to accept a haircut without showing why the offer is better than liquidation or continued default.

Creditors do not need to trust your optimism. They need enough evidence to believe the plan is achievable and worth backing. That is why presentation matters. So does timing. So does the quality of the financial material behind the proposal.

Stage five. Living under the plan

Approval is not the win. Performance is.

Once the plan is accepted, the company has to make the agreed contributions and trade with discipline for the full term of the arrangement. Directors who treat approval as the end of the crisis often end up in trouble again. The same habits that created the pressure the first time can destroy the restructure the second time.

That is why some directors use support around the statutory process, not just inside it. Firms such as LemonAide provide director-focused pre-insolvency and debt advisory support. That can include reviewing the wider business and personal position, helping prepare for the formal process, and assisting with implementation decisions while the practitioner handles the statutory role.

From the director's side, the SBR process is not a formality. It is a compressed test of viability, discipline, and credibility. If you enter it prepared, it can preserve the business and contain personal exposure. If you enter it hoping the process itself will fix weak records or poor decisions, it can fail very quickly.

SBR vs Other Insolvency Options A Director's Choice

A director usually reaches this point under pressure. Cash is tight, creditors are louder, and every option feels expensive in a different way. The key question is not which label sounds safer. The question is which process gives your company a credible chance of survival without exposing you to more personal risk than necessary.

SBR sits in a very different category from voluntary administration and liquidation. If the company is still viable, records are in order, and the business can fund a realistic compromise with creditors, SBR can preserve trading and keep directors in control. If those elements are missing, forcing an SBR often wastes time you do not have.

If you do not qualify for an SBR, reach out to talk to one of LemonAide's qualified representatives about your other alternatives that suit your circumstances.

What the outcomes actually mean for directors

As noted earlier in the article, ASIC's REP 810 report points to strong completion and business survival outcomes for many companies that entered and fulfilled SBR plans. Used properly, that matters. It means SBR is not just a legal shelter while the business deteriorates. It can work as a genuine recovery mechanism.

But directors need to read those outcomes carefully. They do not prove that every distressed small business should restructure. They show that eligible companies with a workable business, current compliance, and disciplined execution can come out the other side intact. That is a narrower group than many generic guides suggest.

The practical comparison

| Feature | Small Business Restructure (SBR) | Voluntary Administration (VA) | Liquidation |

|---|---|---|---|

| Director control | Directors usually remain in day-to-day control while the plan is prepared and put to creditors | Control passes to the administrator | Control ends and the liquidator takes over |

| Core objective | Compromise debts and keep the company trading | Stabilise the company, investigate options, and decide whether a deed or winding up is appropriate | Wind up the company and realise assets for creditors |

| Cost profile | Often more workable for smaller companies that qualify | Commonly more expensive and heavier to run | Costs still apply and can reduce returns from remaining assets |

| Operational impact | Trading can continue with less disruption if handled properly | Operations often become harder, with sharper effects on staff, suppliers, and customers | Business continuity usually ends or shrinks fast |

| Investigation pressure | Still serious, but aimed at supporting a restructure proposal | Formal review begins under external control | Liquidator scrutiny of conduct, records, and recoveries becomes a central feature |

| Best fit | Viable small company with a realistic offer to creditors | Company needing external control, breathing space, or broader restructuring options | Company has no realistic path back to solvent trade |

Where SBR is often the better choice

SBR is usually the stronger option where the business itself still makes sense, but the debt burden has become too heavy to service in the ordinary course. The company may have solid sales, decent margins, and loyal customers, yet still be choking on tax debt, legacy arrears, or the tail-end effect of a rough period.

That is the sweet spot. Directors keep control. The brand is not pushed straight into a public insolvency event with the same shock effect as VA or liquidation. Suppliers and staff often have a better chance of staying on side if the process is prepared properly and the proposal is credible.

From a director's perspective, that control matters. It can also be dangerous if you misread the business. Control only helps when the company is capable of performing under a plan.

Where VA or liquidation may be the better call

Some businesses need external control, not another chance to self-manage under pressure.

VA can make more sense where there are major disputes between stakeholders, serious governance issues, uncertain asset positions, or a need to move quickly under an administrator's authority. It is heavier and more disruptive, but sometimes that is exactly the point. If confidence in management has broken down, a director-led process may not be persuasive to creditors.

Liquidation is often the right call where the business is no longer commercially viable, losses are continuing, records are poor, or further trading is likely to worsen the position. Directors sometimes resist this because it feels like failure. In practice, delayed liquidation can produce the worst outcome of all. More tax debt builds. More creditors go unpaid. Personal exposure can get worse.

We tell directors this plainly. Saving a dead business is not a strategy.

The trade-off directors often miss

The attraction of SBR is obvious. Lower cost than VA in many cases. Less disruption. More control. Better chance of preserving the company than Liquidation.

The hidden burden is compliance and execution.

An SBR only works if the company can meet the entry rules, produce reliable numbers, put forward an offer creditors can accept, and then perform that plan over time. If the books are weak, the tax position is muddled, or the forecast is built on hope rather than evidence, SBR can fail quickly. Directors who enter too late often discover that the legal process did not create viability. It only tested whether viability already existed.

Experienced pre-appointment advice holds practical importance. Director-first advisers such as LemonAide help test whether SBR is suitable before you commit to a formal path, and that can protect both the business and your personal position from a bad call made in panic.

The director's decision standard

Choose SBR if the company is still viable, eligibility is clear, and you can support a realistic proposal with clean records and disciplined trading.

Choose VA if outside control is needed to stabilise the situation or deal with complexity that SBR cannot handle.

Choose liquidation if the business cannot be saved without digging the hole deeper.

Directors lose options by hesitating and by choosing the least confronting process instead of the right one. The right call is the one that matches the facts, contains risk early, and gives creditors a better outcome than the alternatives.

Your Practical Checklist Before Starting an SBR

If you think SBR may be relevant, your first job is not to announce it. Your first job is to get organised. Distressed companies lose options when directors keep trading blind.

Stop the damage first

Before you look at any formal process, stabilise the business.

Freeze non-essential spending: If a cost doesn’t protect revenue, compliance, or core operations, question it.

Stop improvised creditor deals: Side promises made under pressure often create inconsistency and later problems.

Protect records: Don’t let panic produce messy bookkeeping or undocumented payments.

Build a clean information pack

Most directors know less about their real debt position than they think. You need one working file that pulls the facts together.

Accounting file up to date in Xero, MYOB, or your current system.

Bank statements across all accounts.

ATO portal information and a clear tax debt summary.

Aged creditor list and aged debtor list.

Payroll and employee entitlement position showing up to date.

Loan schedules, director loan accounts, and related party balances.

Major contracts, leases, and any litigation or demand letters.

This isn’t busywork. It’s how you find out whether the company can support a formal proposal or whether there’s a deeper structural issue that needs a different response.

Ask the hard commercial questions

Before you spend time and money on a formal pathway, test viability bluntly.

Are sales still real and collectable?

Is margin good enough when pricing is honest?

Are losses caused by debt pressure, or is the business losing money due to its fundamental operations?

Could the company trade normally if historic unsecured debt was dealt with?

If you can’t answer those questions, you’re not ready.

Get advice before the crisis chooses for you

The right early conversation is confidential, practical, and brutally clear. It should cover both the company and your personal exposure, including guarantees, director risk, asset position, and what options remain if SBR isn’t available.

Directors often wait too long because they assume advice starts with surrender. It doesn’t have to. Good pre-insolvency advice starts with preserving optionality, getting facts straight, and making sure you don’t accidentally worsen your position while trying to save the business.

Beyond the Restructure What Happens Next

Creditor approval is a milestone, not the finish line.

What matters next is execution. If the company misses plan payments, falls behind on current obligations, or slips back into poor financial control, the benefit of the restructure can disappear quickly. I’ve seen directors work hard to get a proposal accepted, then lose ground because they treated approval as relief instead of a stricter operating standard.

The better view is simple. An SBR gives the company a second chance to trade properly. It does not fix weak pricing, bad reporting habits, unmanaged tax exposure, or a business model that was already failing before the debt pressure hit.

Completion matters more than approval

Earlier ASIC reporting referenced in this article points to a practical reality. Plans that are completed can support genuine business continuity. That is the outcome directors care about. Keeping the company alive, compliant, and commercially stable.

That result takes work. The post-approval period usually demands tighter controls than the business had before distress, not looser ones.

The seven-year restriction should change your behaviour

One point too many generic guides treat lightly is the seven-year restriction on using the SBR pathway again, as noted earlier in the article.

For directors, that has real strategic weight. If you use this process now, then run back into serious trouble inside that period, this option may not be there to protect the company the second time. That is why we push directors to treat an SBR as a reset point for the whole business, not just a debt compromise.

Use the breathing room to fix the causes, not only the symptoms.

What disciplined directors do after approval

Directors who get through an SBR and stay out of repeat distress usually focus on a few practical areas.

Keep accounts current and readable. If management numbers are six weeks late, you are operating blind.

Stay current on tax, super, and lodgements. Some old debt can be compromised. New non-compliance creates fresh risk.

Protect margin. If your pricing still does not cover labour, overhead, and finance pressure, the restructure has bought time but not solved the problem.

Watch related party dealings and director drawings. Sloppy transactions after approval can create new problems fast.

Review personal exposure. Guarantees, security positions, and asset ownership should be revisited while the company is stable enough to act.

Control growth. New work, new staff, and new sites can strain cash before they produce profit.

This is also the stage where director-first advice matters most. LemonAide works with directors after approval to keep the company on plan, tighten compliance, and assess whether any personal asset protection steps should be considered separately from the company process. That is the part many firms ignore. It is also where avoidable mistakes usually happen.

A completed restructure should leave you with a cleaner balance sheet and a stricter way of running the business. If it only leaves you with less debt, the job is half done.

Frequently Asked Questions about SBR

Does an SBR protect me from personal liability

An SBR can stabilise the company. It does not wipe out your personal exposure.

If you have signed personal guarantees, borrowed in your own name, mixed personal and company funds, or dealt with related entities loosely, those risks sit outside the company compromise and need separate review. Directors get caught here because they assume saving the company also fixes their own position. It does not. We assess both at the same time because a company plan that leaves your personal assets exposed is only half a strategy.

What happens if creditors vote no

If creditors reject the proposal, the plan does not take effect and time is usually the first casualty. Cash keeps tightening, pressure from the ATO or suppliers tends to increase, and your remaining options can narrow fast.

Preparation decides a lot here. A proposal built on weak records, optimistic forecasts, or unresolved creditor issues can fail for reasons that were visible before it went out. Once that happens, you may need to shift quickly into voluntary administration, liquidation, or another turnaround path while there is still something worth preserving.

How much does an SBR really cost

Cost depends on the state of your books, the number of creditors, the quality of your financial records, and how much cleanup is needed before a practitioner can put a credible plan forward.

Practitioner fees are only one part of the spend. Directors often also face accounting catch-up work, cash flow forecasting, legal advice on disputed debts or guarantees, and separate advice on personal risk. Cheap day one advice can turn expensive if the proposal is poorly prepared, rejected, or approved but impossible to complete.

Can I choose which creditors are included

The process applies to eligible pre-appointment unsecured debts under the legal framework. It is not a selective deal where directors decide who gets counted and who gets left out for convenience.

That is a common mistake. If there is a major creditor, a related party balance, or a disputed amount that could affect voting or confidence in the plan, it needs to be addressed properly before documents go out. Mishandling creditor treatment can sink the proposal and raise harder questions about director conduct.

Do I keep running the business during the process

Yes. Directors usually stay in control of trading while the restructure is on foot, with the practitioner overseeing the process and the proposal.

That control is useful, but it cuts both ways. You still need clean records, disciplined cash handling, current reporting, and a clear explanation for unusual transactions. If the business keeps trading badly during the process, staying in the chair becomes a risk, not a benefit.

Is SBR only for ATO debt

No. Tax debt often drives the conversation, but SBR can deal with a broader mix of unsecured liabilities, including supplier debt and other ordinary unsecured claims.

The better question is whether the business can trade profitably after the old debt burden is compromised. If the core business still loses money, the debt type matters less than directors hope.

What if my business has unpaid employee entitlements

This needs attention early as if it remaions unpaid it is an automatic disqualifier if it is due and payable and not paid prior to the appointment of a Small Business Restructuring Practitioner.

Is SBR always the right move if I’m eligible

Eligibility only means you can consider the pathway. It does not mean the business is viable or that SBR is the best option.

Some companies need a different form of restructuring. Some should stop trading before losses deepen further. Some directors need to focus first on personal guarantees, asset exposure, and whether continuing to trade creates more risk than value. That is why we push for a director-first review before any appointment. The company position matters, but your position matters too.

If you’re weighing up a small business restructure sbr and need a director-focused review of both the company and your personal position, LemonAide offers confidential pre-insolvency and debt advisory support across Australia. Start with a clear assessment of viability, eligibility, risk areas, and the alternatives before a creditor or cash flow crisis makes the decision for you.