What Is Voluntary Administration in Australia?

When you’re staring down the barrel of a financial crisis, it’s easy to feel like the walls are closing in. Creditors are calling non-stop, cash flow has all but evaporated, and terms like voluntary administration start getting thrown around. But what does it actually mean?

Let's cut through the jargon. Voluntary administration is a formal process under Australia's Corporations Act 2001. It's designed for a struggling company that might still be viable, giving it a chance to restructure and survive.

What Is Voluntary Administration?

Think of it as hitting a giant ‘pause’ button. When your board of directors decides the company either is, or is likely to become, insolvent (meaning it can't pay its debts as they fall due), they can appoint an independent, qualified insolvency practitioner to step in as the administrator. This single move provides immediate, powerful breathing room.

The moment the administrator is appointed, a moratorium kicks in. This is a legal freeze on most claims from creditors. Unsecured creditors, landlords, and even the ATO are generally stopped in their tracks, unable to start or continue legal action to chase their money. This freeze buys the administrator time to take complete control of the company and dive deep into its financial affairs.

The core purpose of voluntary administration is to maximise the chances of the company, or as much of its business as possible, continuing to exist. If that's not possible, the goal shifts to achieving a better return for creditors and members than would result from an immediate winding up of the company.

Crucially, this isn't an instant death sentence for your business. It’s a structured pathway to find the best possible outcome for everyone involved. But make no mistake: it’s a formal and expensive process that takes all control out of your hands as a director. An alternative, like working with LemonAide, allows you to explore private solutions first, which can often save the business without the need for this drastic public step.

To get a clearer picture, it helps to see how voluntary administration stacks up against going straight into liquidation.

Voluntary Administration vs Direct Liquidation At a Glance

The choice between these two paths comes down to your primary goal: are you trying to save the business, or is it time to close the doors for good? This table breaks down the key differences.

| Aspect | Voluntary Administration | Direct Liquidation |

|---|---|---|

| Primary Objective | To rescue and restructure a viable business, or parts of it. | To wind up the company's affairs and cease operations. |

| Control | The administrator takes full control. Directors lose their powers. | The liquidator takes full control. Directors lose their powers. |

| Potential Outcomes | Deed of Company Arrangement (DOCA) with control of the company returning to directors, in very rare circumstances the Voluntary Administration ends again with control of the company returning to the directors or liquidation. | Dissolution of the company after assets are sold and distributed. |

As you can see, voluntary administration is built around the possibility of a comeback. Liquidation, on the other hand, is the end of the line for the company. Working with a service like LemonAide before making either choice can help you determine if a private rescue is possible, which is a far better alternative than both formal options.

The Recent Surge in Formal Appointments

It's not just you. More and more businesses are being forced into formal insolvency processes like voluntary administration. As the economy tightens and the ATO ramps up its debt collection, the pressure on directors is immense.

Recent data paints a stark picture: in the 12 months to March 2024, a total of 10,268 insolvency appointments were recorded. That's a staggering 53% increase from the previous year, showing just how tough the current environment is. You can dig into the full corporate insolvency report here for a deeper dive into these trends.

The Smarter Alternative to a Formal Mess

While voluntary administration has its place, it's a reactive move made when a crisis has already hit boiling point. A much smarter path is to engage a pre-insolvency specialist like LemonAide before things get that dire.

We work for one person: you, the director. Our job is to find private, confidential, and director-controlled solutions. This could mean informal creditor negotiations, a quiet strategic restructure, or other options that keep you in the driver's seat and avoid a public, formal appointment altogether.

Acting early with LemonAide opens doors that an administrator—who is legally bound to act for all creditors—simply cannot. It's the difference between being tossed about by the waves and having an experienced navigator help you steer through the storm with a clear plan.

A Step-by-Step Look at the Voluntary Administration Process

Going into voluntary administration can feel like you’ve been thrown into a legal maze with no map. Getting your head around the process, the timeline, and what happens at each stage is the first step to finding your way out. It’s a very formal process, but knowing what’s coming allows you to plan your moves instead of just reacting to what’s thrown at you.

An independent administrator runs the whole show, and their job is to get the best result for all the creditors. But here’s the thing: before you go down this very public and stressful path, a quiet chat with a director-focused advisor like LemonAide can open up private options you didn’t know you had. If there's no other way forward, we make sure you walk into administration prepared and from a position of strength, not desperation.

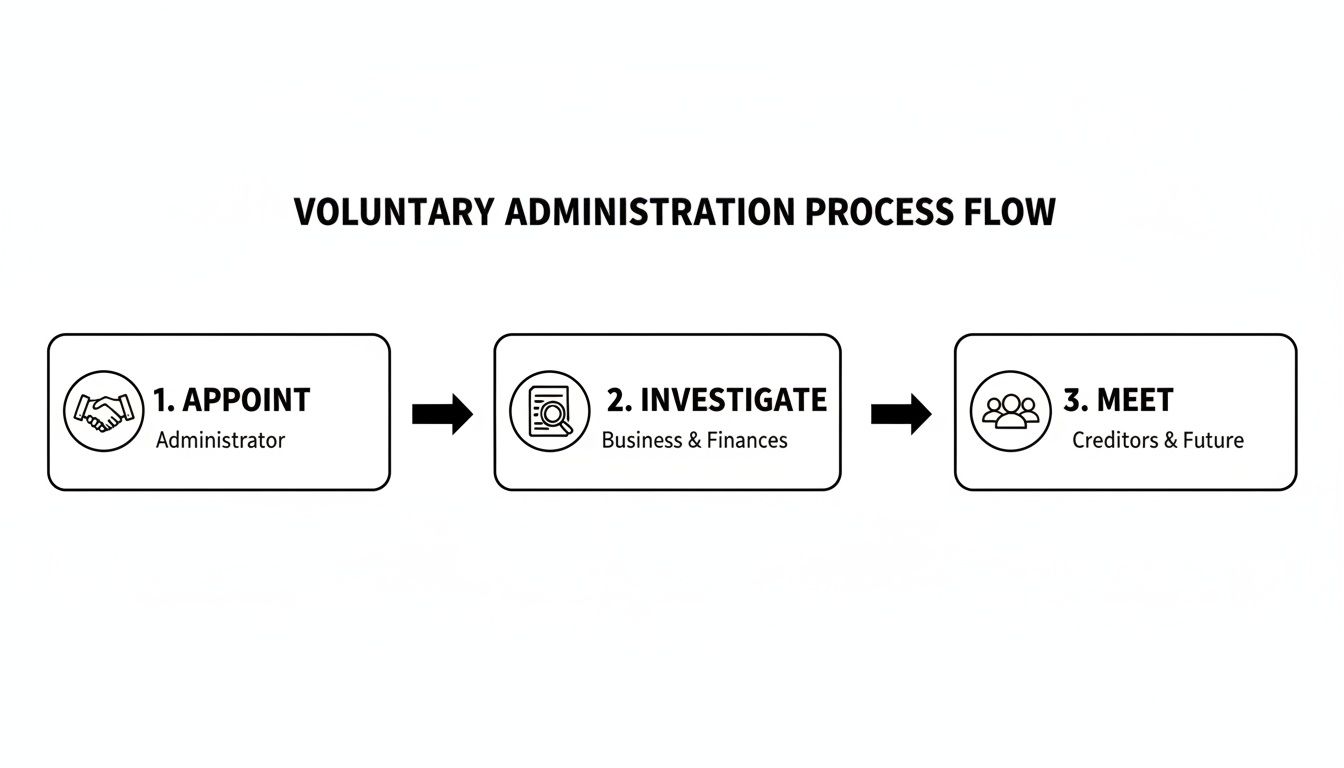

Stage 1: The Appointment and the "Time-Out"

It all officially starts when the company's directors, seeing that the business is insolvent (or about to be), make the call to appoint an administrator. This is a huge decision. From that moment, you hand over the keys to the entire kingdom—the company, its bank accounts, assets, and day-to-day operations—to this outsider.

At the moment an administrator is appointed, a legal shield called a moratorium slams down. Think of it as a mandatory "time-out" for anyone you owe money to. This freezes most unsecured creditors in their tracks, stopping them from starting or continuing any legal action to chase their debts. It’s designed to give the administrator some much-needed breathing room to figure out what’s going on without being hounded by legal threats.

Stage 2: The Administrator's Investigation

With that time-out in effect, the administrator rolls up their sleeves and starts digging into the company's finances. They’ll take control of all your books and records, pour over cash flow statements, list out every asset, and put past transactions under a microscope. Their mission is to get a complete, unvarnished picture of the company’s business, property, and financial state.

As a director, you're legally required to give them all reasonable help. This means handing over every record and piece of information they ask for. But remember, while the administrator is meant to be neutral, their primary focus is the company and its creditors. This is where having LemonAide in your corner makes a massive difference—we represent you, helping you understand your obligations while fiercely protecting your personal interests during this intrusive phase.

A key part of the administrator's job is to form an opinion on three possible futures: review the proposed Deed of Company Arrangement (DOCA), in very rare circumstances end the administration and give the company back to the directors, or wind the company up through liquidation. Everything they uncover in their investigation is building towards the final recommendation they'll make to creditors.

Stage 3: The First Creditors' Meeting

This meeting is usually held within eight business days of the appointment and is mostly for show-and-tell. The administrator will introduce themselves, confirm they've been appointed, and give a quick rundown of what they’ve found so far.

Creditors really only have two big decisions to make here:

Form a Committee of Inspection: They can vote to create a small committee that will work more closely with the administrator and act as a voice for all the other creditors.

Replace the Administrator: If the creditors aren't happy with the administrator the directors chose, they have the power to vote them out and bring in their own registered administrator.

Stage 4: The Second and Final Creditors' Meeting

This is the big one. Usually held around 20-25 business days into the process, this is where the company’s fate is ultimately decided. Before the meeting, the administrator sends out a detailed report to every creditor.

This crucial report spells out:

What their investigation uncovered.

The company’s true financial position.

The administrator's opinion on the three possible outcomes (DOCA, end the voluntary administration, or liquidation).

Their recommendation for which path they believe will give creditors the best return.

At this meeting, the creditors vote on what happens next. The administrator's recommendation carries a lot of weight, but the final call belongs to the creditors. This is exactly why a solid game plan before you even enter voluntary administration is so vital. By working with LemonAide beforehand, we can help you build a viable proposal for a Deed of Company Arrangement (DOCA), massively improving the odds that creditors will vote to save your business instead of killing it off.

Understanding the Administrator's Role and Director Duties

When your company enters voluntary administration, the power shift is immediate and absolute. Think of it like someone else being handed the keys to your car, your house, and your bank account all at once. The administrator isn't just an advisor; they become the company's new controlling mind.

From the second they're appointed, the administrator takes full control of everything: the business, its assets, the bank accounts, and all operational decisions. Your power as a director is effectively put on ice. You can't sign contracts, make payments, or manage the company's affairs any longer.

The Administrator's Powers and Primary Duty

The administrator is a registered liquidator, an independent professional with sweeping powers under the Corporations Act 2001. Here's the crucial part: their fiduciary duty is not to you. It's to the company and, more importantly, its creditors. Their job is to get the best possible outcome for the creditors as a group.

This means they will:

Investigate the company’s affairs: They'll dig deep into the business's history, its finances, and what went wrong.

Take control of assets: They manage, protect, and can sell company assets to maximise the money available for creditors.

Run or wind down the business: They have the authority to keep trading if they think it helps the chances of a successful restructure, or they can shut the doors immediately.

Report to creditors: They must provide detailed reports to creditors and call meetings to decide the company’s fate.

This infographic breaks down the core stages the administrator will steer the company through.

It looks simple enough, but each step is managed by the administrator, a neutral party whose job is to follow the rulebook. In contrast, using LemonAide allows you to explore director-led alternatives that keep you in control and avoid this formal, public process altogether.

Your New Role: Your Director Duties

Just because your decision-making powers are gone, don't think your duties have vanished with them. You now have a legal obligation to provide "all reasonable assistance" to the administrator. This is non-negotiable.

Your legal duty during voluntary administration is to cooperate fully. This means handing over all company books and records, showing up to meetings, and answering any questions the administrator has about the company's business, property, or transactions. Failing to cooperate can lead to serious penalties.

This can feel incredibly confronting. You're legally required to help someone who is actively investigating your past actions, including looking for potential insolvent trading. It's a common point of stress for directors, especially when you're worried about personal assets. If you want to know more, you might find our guide on what happens to a director when a company is liquidated useful.

The Critical Difference: LemonAide Is on Your Side

This is the most important thing you need to grasp: the administrator is neutral, but we are not. The administrator works for the benefit of all creditors. We work exclusively for you.

While the administrator is busy digging through the company’s past, our focus is squarely on protecting your future. We act as your private, strategic advisor, making sure your interests don't get bulldozed in the process.

Here’s what having an advocate like LemonAide in your corner really means:

Strategic Communication: We help you manage every conversation with the administrator, ensuring you meet your legal obligations without accidentally putting your personal assets at risk.

Liability Defence: We prepare you for the investigation and work to defend you from personal liability claims, including nasty insolvent trading allegations.

Rights Protection: We make sure your rights as a director are respected every step of the way.

Proposal Development: We can help you put together a viable Deed of Company Arrangement (DOCA) proposal that gives your business the best chance of survival and protects you.

An administrator simply cannot offer this kind of personal advocacy; their role forbids it. Think of them as the referee, focused on enforcing the rules of the game for everyone. We're your coach, working with you to build the winning strategy before you even step onto the field.

What Are the Possible Outcomes of Voluntary Administration?

The whole point of voluntary administration is to force a decision. That intense period of investigation, negotiation, and frantic activity all comes to a head at the second creditors’ meeting. This is where the company’s fate is decided.

When it all shakes out, there are really only three ways this can go.

Knowing what these outcomes mean in the real world is everything. It’s the difference between saving your business, watching it get broken up and sold, or—in very rare cases—getting the keys back. This is where directors who’ve planned ahead have a massive advantage. Hoping for the best usually leads to the worst, but walking in with a solid strategy from a service like LemonAide can completely change the game.

Outcome 1 The Deed of Company Arrangement (DOCA)

This is the goal for most directors wanting to save their business. A Deed of Company Arrangement, or DOCA, is a formal deal struck between the company and its creditors. It’s a binding compromise that lets the business keep trading while settling its debts, usually for a better return than creditors would see from a fire-sale liquidation.

Think of it as a negotiated financial reset for the company.

A DOCA lays out a new set of rules. Typically, it will involve things like:

Creditors agreeing to accept a partial payment, like a certain number of cents in the dollar, over a set period.

A "time-out" on payments, giving the company breathing room to get its finances in order.

The sale of specific, non-essential assets to raise funds for the deal.

Once creditors vote 'yes' on the DOCA, the voluntary administration officially ends. The DOCA document is prepared and executed and then control is then handed back to the directors (or a new owner) to run the business under the agreed terms.

The Power of Pre-Insolvency Planning

A successful DOCA doesn't just happen. Creditors are not going to agree to a deal out of the goodness of their hearts; they need a commercially sound proposal that shows them they'll get more money back this way than any other. This is precisely why getting a specialist like LemonAide involved before you even appoint an administrator is a game-changer.

We work with you to build a compelling DOCA proposal before the clock even starts ticking. By having a fully-baked plan ready to go, you enter the process from a position of strength, not scrambling in desperation. This dramatically increases the chances that the administrator will recommend your proposal and that creditors will vote for it.

Outcome 2 End the Voluntary Administration

This is the unicorn of voluntary administration outcomes—it’s incredibly rare. It only happens if the administrator digs into the company’s books and finds that it was actually solvent the whole time. If that’s the case, the administration ends, and the company is simply handed back to the directors to carry on as if nothing happened.

This path is almost unheard of. A company enters voluntary administration because it's believed to be insolvent. To prove it was solvent all along usually means the initial appointment was a mistake or the result of a temporary, ill-advised panic.

While it sounds ideal, its rarity means you absolutely cannot bank on this happening. It’s a stark reminder of why getting accurate financial advice early on from a service like LemonAide is so critical to understanding your true solvency position in the first place, potentially avoiding this formal process entirely.

Outcome 3 Liquidation

If creditors vote down a DOCA proposal, or if no realistic deal is ever put forward, the default outcome is liquidation. At that second meeting, creditors will vote to wind up the company, and the process flips immediately from a potential rescue to a final shutdown.

The administrator typically just changes hats and becomes the liquidator. Their job is no longer about saving the business; it's about closing it down in an orderly way. They will sell off every company asset, chase any potential claims (like insolvent trading against directors), and distribute whatever money is left to creditors in a strict order of priority. For the company, this is the end of the line.

The construction industry has seen far too much of this outcome lately. Between May 2024 and May 2026, the sector was hit with a wave of failures, with 2,636 construction companies becoming insolvent in the 12 months to March 2026 alone—a massive 23% jump from the year before. You can learn more about the building industry insolvency crisis and see why it’s a brutal lesson in the need for early, strategic advice. Without a plan, liquidation is almost inevitable. A better alternative is getting advice from LemonAide to attempt a private workout or restructure, which can prevent liquidation.

Protecting Your Personal Assets from Business Debts

For any director staring down the barrel of financial trouble, one question screams louder than all the others: "What about my house?" The fear of losing the family home or your life savings because the business went under is a heavy weight to carry. It’s also one of the main reasons so many directors put off asking for help.

So let’s be crystal clear about what voluntary administration can—and can’t—do to protect your personal assets.

There’s a dangerous myth that putting your company into voluntary administration throws an automatic shield around your personal wealth. It absolutely does not. Voluntary administration is a process designed for the company, not for you as an individual director. It doesn't magically wipe out any personal liabilities you've racked up.

The "corporate veil" is supposed to separate a company's finances from a director's personal life. But that veil can be pierced. Things like personal guarantees, director loans, and ATO director penalty notices can punch right through it, putting your personal assets squarely in the firing line.

If you’ve signed a personal guarantee for a business loan, for instance, that creditor can come after you directly for the debt. The company being in administration won't stop them. This is one of the biggest risks directors face, and you can learn more about what can happen with personal guarantees in our detailed guide.

When Business and Personal Debts Collide

The line between business debt and personal debt can get dangerously fuzzy, fast. According to the Australian Financial Security Authority (AFSA), there were 1,169 new personal insolvencies in September 2024 alone. Even more telling is that 350 people who entered personal insolvency in March 2024 were also involved in businesses, often in sectors like construction and transport. You can explore more statistics on personal insolvency from AFSA.

This is where the standard insolvency process just doesn’t cut it for directors. An administrator is appointed to the company. Their legal duty is to focus only on the company’s affairs and get the best result for creditors. They have zero obligation to advise you on your personal exposure. In fact, their investigation might actually dig up reasons to come after you personally.

The LemonAide Difference: A True Firewall

This is exactly the gap LemonAide was built to fill. An administrator can only deal with the company, but we look at your entire financial picture—both business and personal. Our one and only job is to protect you.

We offer a service that an Administrator simply can't. We analyse your whole situation to build a complete strategy that deals with the company’s debts while creating a legal firewall to protect your personal wealth.

Here’s how our process works:

A Full Analysis: We dive deep into your company structure, personal guarantees, any director loans, and your ATO liabilities.

Asset Protection Strategy: We find the legal pathways to safeguard your family home and other personal assets from creditors.

Negotiation Support: We can negotiate on your behalf, not just for the company, but for your personal liabilities as well.

This approach gives you a single, integrated plan to manage the crisis. You get a strategy for the business and, just as importantly, a shield for your family.

Exploring Better Alternatives to Voluntary Administration

When your company hits financial trouble, it's easy to think voluntary administration is your only option. It’s the name everyone knows, and it can feel like the only lifeline being thrown your way.

But here’s the thing we’ve seen countless times: it’s often the last, most public, and expensive resort. It’s a reactive move that means you’re handing the keys to your business over to a complete stranger, the administrator, who then dictates its future.

The smarter play is almost always to get on the front foot with a service like LemonAide. There are director-led alternatives that keep you in control. These are private, often far more effective solutions that you can only access by seeking advice before a crisis hits. It’s the difference between being a passenger bracing for a crash and grabbing the wheel with an expert navigator riding shotgun.

Informal Workouts and Private Negotiations

Long before you need to google what is voluntary administration, you have the option of a private negotiation. We find that many disputes with creditors, including the Australian Taxation Office (ATO), can be sorted out with an informal workout. This is simply a confidential negotiation process that you manage, with our expertise to back you up.

Instead of a formal, public process governed by rigid legal rules, we help you:

Build a payment plan proposal that is actually realistic and affordable for your business.

Put your case forward to the ATO and other creditors professionally.

Negotiate a compromise that lets your business keep trading, without the black mark of a formal insolvency appointment against its name.

This approach is faster, cheaper, and crucially, keeps your financial challenges out of the public eye. It helps preserve the business relationships you’ve built and gives you the flexibility to find a resolution that actually works. With LemonAide, this becomes a far more effective and less stressful alternative to formal administration.

You can think of it like this: Voluntary administration is major surgery performed in a public operating theatre. An informal workout with LemonAide's help is like seeing a specialist for targeted treatment behind closed doors—often avoiding the need for that surgery in the first place.

The Small Business Restructuring Process

If you run an eligible small business, there’s another powerful tool at your disposal called Small Business Restructuring (SBR). This was introduced as a streamlined process designed to be quicker and less expensive, with one huge advantage: directors stay in control of the company.

Unlike voluntary administration, where an administrator takes charge from day one, the SBR process lets you keep running the business day-to-day. You work alongside a restructuring practitioner to put a formal proposal to your creditors, which they then vote on. LemonAide can help you navigate this process, ensuring it's the right fit and giving you the best chance of a successful outcome, making it a superior alternative to voluntary administration for eligible businesses.

Strategic Corporate Restructuring

Sometimes the best path forward involves more than just a payment plan. It requires making targeted, strategic changes to your company's structure. This isn't about giving up; it’s about being smart to protect your valuable assets and allow the profitable parts of your business to thrive.

A strategic corporate restructure might involve setting up a new company to acquire the healthy parts of the old one, or changing the ownership structure to legally shield key assets from creditors. You can read more in our guide on corporate restructure.

By getting advice from us at LemonAide early on, we can map out these kinds of sophisticated strategies. These are options an administrator simply can't offer you, and they can be the key to securing your financial future while still responsibly dealing with legacy debts.

We Get Asked These Questions a Lot

When you're staring down the barrel of voluntary administration, your head is probably swimming with questions. It’s a complex space, and the answers aren't always straightforward. Here are some of the most common questions we hear from directors in your shoes, with the no-nonsense answers you need.

How Much is This Going to Cost Me?

Let’s be blunt: voluntary administration is expensive. The costs are significant and they come straight out of the company’s assets. An administrator charges for their time, and those fees can easily spiral into tens of thousands of dollars, even for a smaller business.

Every dollar paid to the administrator is a dollar that can't go to your creditors. It's one of the biggest reasons we always tell directors to explore more affordable, private options with an advisor like LemonAide first. Our services are designed to be a far better value alternative, often achieving a better result for a fraction of the cost of a formal appointment.

Can I Keep Working in the Business?

Once an administrator steps in, you, as a director, lose control. All decision-making power is gone. That said, the administrator isn't a magician; they don't know your business like you do.

It’s common for them to ask you to stay on and help run the day-to-day operations. But make no mistake, your role changes completely. You’re essentially an employee taking orders from them, not the one calling the shots. This is a key reason why director-led alternatives offered by LemonAide, like informal workouts or Small Business Restructuring, are a better option as they keep you in control.

Will This Stop the ATO Chasing Me?

Yes, appointing an administrator triggers an immediate freeze (a moratorium) on most actions from unsecured creditors. This includes the ATO, putting a stop to recovery actions like garnishee notices against the company.

However—and this is a big one—it doesn't automatically protect you from personal liability under a lockdown Director Penalty Notice (DPN).

It's critical to understand that the freeze on ATO action is only temporary. An administrator can’t give you personal advice as they have a fiduciary duty to the comapny's creditors. A pre-insolvency advisor like LemonAide, on the other hand, can work with you to build a strategy to tackle that DPN head-on, which is a far better and more complete solution.

Can I Propose My Own Deal (DOCA)?

Absolutely. As a director, you can—and often should—put forward a Deed of Company Arrangement (DOCA). This is your proposal to creditors for a way to save the business and pay back a portion of the debt.

But a flimsy, poorly thought-out proposal will be dead on arrival. Creditors will reject it in a heartbeat. Your best shot at getting a DOCA across the line is to have a commercially viable, watertight proposal developed before you even enter administration. This is where LemonAide can make all the difference, helping you build a compelling case that an administrator will actually recommend and creditors will be willing to accept.

What If I Don’t Cooperate with the Administrator?

Simply put: don't do it. Failing to cooperate is a serious offence under the Corporations Act 2001. You are legally required to hand over all company books and records and provide any reasonable assistance they ask for.

Being difficult won’t help you. It will lead to liquidatation of the company as the administrator can not properly evaluate your DOCA proposal against a potential liquidation and it will definitely put your conduct as a director under a very negative spotlight. Having LemonAide on your side can help you manage these interactions, ensuring you cooperate fully while still protecting your personal position.

Feeling overwhelmed by all this is completely normal. But you don't have to figure it out on your own. The single best thing you can do right now is get expert advice before you're backed into a corner. The team at LemonAide offers a free, confidential chat to give you a clear roadmap, help protect your personal assets, and look at private solutions that keep you in control. Take the first step toward a fresh start and visit www.lemonaide.com.au today.