Your Guide to Dissolve a Company in Australia for 2026

Deciding to close your company is a tough call for any director. It’s a decision loaded with stress and uncertainty. But the biggest mistake I see directors make is choosing the wrong path right at the start, often because they don't fully understand one critical detail: their company's solvency.

Getting this wrong isn't just a simple mistake; it can have dire consequences. Navigating this alone is a recipe for disaster, but specialist advice from a firm like LemonAide provides a clear, safe path forward.

Is It Time to Shut Down Your Company in Australia?

When you're facing the end of your company's journey, the pressure can be immense. Many directors, hoping for a quick and cheap exit, opt for a simple deregistration when, in reality, their company has outstanding debts. This is a massive, and all-too-common, error that can come back to bite them personally.

The first and most critical step is to understand the legal difference between winding down a solvent business and the formal, regulated processes required when you're insolvent. In Australia, there are four main pathways to close a company. Each is designed for a very specific financial situation, and picking the right one is not optional—it's the law.

Four Paths to Dissolve a Company in Australia

Here's a quick rundown of the main methods. The path you take is dictated entirely by whether your company can pay all its debts.

| Dissolution Method | Best For | Key Requirement | Typical Cost |

|---|---|---|---|

| Voluntary Deregistration | Clean, debt-free companies that have stopped trading. | Company is solvent, has assets under $1,000, and all liabilities paid. | $50 ASIC fee |

| Members’ Voluntary Liquidation (MVL) | Solvent companies needing to wind up formally, often to distribute assets to shareholders tax-effectively. | Declaration of Solvency signed by directors. | $3,000 – $10,000+ depending on complexity |

| Creditors’ Voluntary Liquidation (CVL) | Insolvent companies where directors decide to wind up to manage debts and creditor obligations. | Company cannot pay its debts as they fall due. | $5,500 – $22,000+ |

| Court Liquidation | Insolvent companies forced into liquidation by a creditor (like the ATO) via a court order. | A creditor proves the company's insolvency to the court. | Costs vary significantly, often borne by the company's assets. |

As you can see, the options diverge significantly in cost and complexity. Navigating this alone is a minefield. This is precisely where getting specialist advice early on saves you from disaster.

A firm like LemonAide doesn't just push you into a predetermined process. Their first step is a free, no-strings-attached review to analyse your company's true financial health and explore alternatives you might not even be aware of. This is a far better alternative than guessing your way through the process and hoping you've made the right call.

Before you get locked into a costly or damaging process, an experienced advisor can help you understand your real situation, assess your personal risks, and choose the right strategy from the outset.

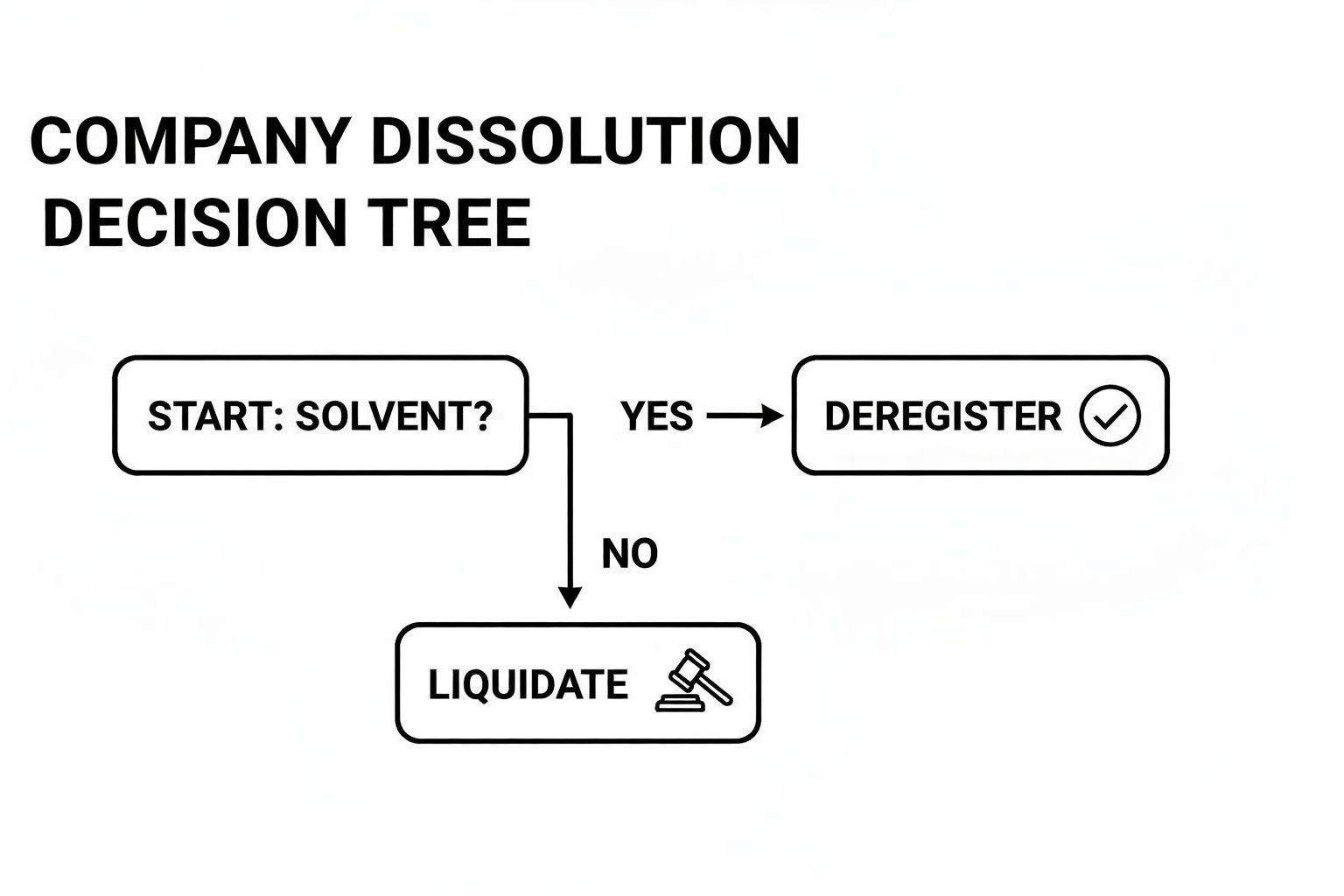

Why Solvency Is the Deciding Factor

The infographic below shows the simple but critical fork in the road every director faces.

As you can see, the first question—is the company solvent?—sends you down one of two completely different paths: a simple deregistration or a formal liquidation.

This isn’t a decision to be made on a gut feeling. Australian law has very strict definitions of solvency, and getting it wrong can have severe consequences. Under the immense stress of a failing business, many directors simply don't have a clear picture of where their Company truly stands or how it may relate to their personal financial position.

The numbers tell a stark story. In the 2023-24 financial year, over 12,500 external administrations were initiated in Australia—a 20% jump from the year before. With small businesses making up 97% of all companies, and around 60% failing within the first three years, it's clear that many directors end up in a Creditors' Voluntary Liquidation. For more context, you can explore the latest statistics on business failure rates.

This is exactly where LemonAide’s expertise becomes your lifeline. Their service is built for directors in this exact situation. They conduct a thorough review to take the guesswork out of determining your solvency. From there, they map out the safest and most effective strategies available, ensuring you don't accidentally step on a legal landmine. It’s a far better approach than guessing and hoping for the best.

The Clean Exit: Solvent Company Deregistration

So, your company has run its course. You’ve paid every last creditor, wrapped up operations, and there's not much left in the bank. For a business like this, a voluntary deregistration is often the cleanest and cheapest way to shut the doors for good. It's the simple exit ramp for solvent companies that have reached the end of their life without any financial drama, as long as their are no contingent liabilities in the future, such as a warranty for repair work on a new building.

But "simple" doesn't mean you can just walk away. The Australian Securities and Investments Commission (ASIC) has a very strict checklist. Get it right, and it’s a smooth, final end. Get it wrong, and you could find yourself in a world of trouble you thought you’d left behind.

Meeting ASIC’s Criteria for Deregistration

Before you can even think about applying to ASIC, your company must meet a few non-negotiable conditions. It can't be mostly wound up; it has to be completely finished, debt-free, and dormant.

Here’s what ASIC demands:

Universal Agreement: The majority of members (shareholder) in value must agree to deregister the company.

Ceased Operations: The company must have stopped trading and is no longer carrying on any business.

Asset Limit: The company’s assets must be worth less than $1,000.

No Outstanding Debts: This is the big one. The company must have zero liabilities. That means no money owed to suppliers, landlords, or lenders, and definitely no outstanding obligations to the Australian Taxation Office (ATO).

No Legal Proceedings: The company can’t be involved in any court cases or legal disputes.

Once you’ve ticked all these boxes, the final step is for the directors to lodge an Application for voluntary deregistration of a company (Form 6010) with ASIC and pay the deregistration fees.

The Deregistration Trap a Director Cannot Afford to Fall Into

Because it’s cheap and looks easy, deregistration is a tempting option. But it’s also a massive trap for directors of companies with unresolved or hidden debts. I’ve seen directors try to use it as a shortcut, thinking that dissolving the company makes its liabilities magically disappear. This is a critical and incredibly costly mistake.

A creditor, especially the ATO, can apply to have a deregistered company reinstated. When this happens, the company is treated as if it was never dissolved. Directors can then be personally chased for debts they thought were long gone.

Think about this real-world scenario: a director of a small construction company deregisters it, assuming a big supplier debt will just be written off. Six months later, the supplier gets a court order to reinstate the company and then requests that the court to liquidate the Company. The director may then be found liable for insolvent trading, and the "corporate veil" offers zero protection. Suddenly, their family home is on the line.

This is exactly where getting proper advice from a firm like LemonAide is worth its weight in gold. Instead of you just hoping you’re solvent, they do a proper check to confirm you genuinely qualify. This protects you from the massive legal and financial fallout of getting it wrong.

While voluntary deregistration is a popular low-cost exit, with around 25,000 companies deregistered in 2023-24, the requirements are strict, and approximately 15% of applications are rejected for non-compliance. For distressed directors, confusing this process with insolvency relief can be disastrous; 22% of Directors face bankruptcy after personal guarantees are called upon. You can explore further research on why getting early, expert advice is crucial.

Using LemonAide's service is a better alternative because they don't just point out red flags. They give you a clear, legal strategy to fix them, making sure that when you do dissolve your company, it’s a final end to that chapter—for good.

Navigating Liquidation When Debts Are Unmanageable

When your company’s debts are piling up and you can’t see a way to pay them, you've likely crossed the line into insolvency. At this point, the clean and simple option of deregistration is gone. The only path forward is liquidation. It’s a tough reality to face, but burying your head in the sand is the worst thing you can do.

Ignoring the problem doesn’t make it go away; it just dramatically increases your personal risk. For an insolvent company, there are really only two ways this ends: a Creditors' Voluntary Liquidation (CVL) or a Court Liquidation. Both wind up the company, but how you get there makes a world of difference for you as a director.

You Initiate a Creditors’ Voluntary Liquidation

A CVL is the path you, the director, choose to take. It’s what happens when you and your board look at the numbers and have to admit the company is insolvent and can’t keep trading. You make a formal resolution to put the company into liquidation and appoint a liquidator to take over the company.

This is the proactive, responsible move. By starting a CVL, you’re doing your duty as a director to stop the company from trading while insolvent. But here’s the catch, and it’s a big one: once that liquidator is appointed, they do not work for you. Their legal fiduciary duty is to the company's creditors.

Their job is to sell off company assets, dig through the company’s history (including every recent decision you made), and pay out whatever they can to the people you owe money to. It can feel like you’ve lost all control, forced to watch from the sidelines as your business—and your conduct—is put under a microscope.

Creditors Force a Court Liquidation

The alternative is a whole lot worse. If you do nothing, your creditors will eventually force your hand. Usually, a creditor who has run out of patience—very often the ATO—will apply to the court for an order to have your company wound up.

A court liquidation is a defensive, reactive position you never want to be in. It sends a clear signal to the court, the ATO, and every other creditor that you may have failed to act responsibly. The court-appointed liquidator is often far more aggressive as their fees are paid AFTER the petitioning creditors costs, and your personal risk for things like insolvent trading goes through the roof.

You lose control of the timing, the narrative, and the process. Instead of managing an orderly exit, you’re dragged through it.

This is where directors have a crucial, but brief, window of opportunity. Before you hand the keys to a liquidator who is legally bound to act for your creditors, you have a moment to get your own house in order. This is where pre-insolvency advice isn’t just a good idea—it’s your single best line of defence.

Shifting the Power Back to You with Pre-Insolvency Advice

This is exactly where a specialist like LemonAide steps in. They work for you, and only you. They are not liquidators; their job is to be your advocate before the formal liquidation process even starts.

They act in that critical gap between you realising the company is in trouble and you appointing a liquidator. Their entire focus is on you, their client. They analyse your specific situation to spot the risks—personal guarantees you’ve signed, potential insolvent trading claims—and build a strategy to minimise them. This often involves:

Asset Protection: Looking at how your personal assets, especially the family home, are structured and finding legal ways to shield them.

ATO Negotiations: Dealing with the ATO on your behalf to manage Director Penalty Notices (DPNs) and negotiate payment arrangements.

Managing Director Duties: Guiding you to take the right, documented steps to show you’ve acted responsibly, which significantly reduces your personal liability risk.

In Australia, a Creditors' Voluntary Liquidation is the most common end for an insolvent company. There were 8,200 of them in the year to June 2024, accounting for 65% of all formal insolvencies. In New South Wales alone, 2,900 companies were wound up in 2024, and directors were often hit with personal liability for insolvent trading, with penalties averaging $45,000 per case. As studies show, this can easily lead to personal bankruptcy, but good pre-insolvency advice can stop that from happening.

Working with LemonAide improves your situation because you go into the liquidation process prepared and from a position of control. You've already dealt with your personal risks and have a clear plan. Instead of being blindsided by a liquidator's investigation, you’ll have a clear record of responsible action, guided by expert advice. It turns a scary, uncertain process into a managed one. To get a better feel for the mechanics, have a look at our detailed guide on what happens during a liquidation.

Director Duties and Personal Risks You Cannot Ignore

When you run a company, you operate under the assumption that the "corporate veil" protects you. It’s meant to be a legal wall between the business’s debts and your personal assets. But when a company gets into financial trouble and starts heading towards dissolution, that veil can get dangerously thin.

In some situations, it can be ripped away entirely. This leaves you, the director, personally exposed to all the financial fallout.

Suddenly, every decision you’ve made comes under a microscope. This isn't just about the company's survival anymore—it's about protecting yourself and your family. Once a liquidator is appointed, they have a legal duty to investigate why the company failed, and that investigation will point squarely at your actions as a director.

The Danger of Insolvent Trading

The biggest landmine for any director of a struggling company is insolvent trading. It’s a concept that trips up so many people. Under Australian law, you have a strict duty to stop your company from taking on new debts if it's already insolvent, or if incurring that debt would push it over the edge.

It sounds simple, but think about what it means in practice. Continuing to trade—ordering more stock, hiring contractors, taking on that new project you hope will turn things around—when you know (or really should have known) you can't pay for it is a serious breach of your duties.

If a liquidator uncovers evidence of insolvent trading, they can sue you personally to recover money for the creditors. This isn’t a company debt anymore; it becomes a personal liability that can lead straight to your own personal bankruptcy.

Personal Guarantees: The Ghost of Debts Past

I’ve seen this happen countless times, especially with small to medium-sized businesses. To get finance for a new piece of equipment, a business loan, or even just the lease on your office, you had to sign a personal guarantee. At the time, it probably felt like a bit of paperwork. A formality.

But when you liquidate a company with outstanding debts, those guarantees spring back to life with a vengeance.

The moment the company is liquidated, the bank or landlord will come directly to you to make up the difference. That business loan you signed for? It's your personal problem now. The outstanding account with that creditor? You're on the hook for every dollar. Personal guarantees are designed to bypass the corporate veil completely.

A liquidator's has a fiduciary duty to act for the company's creditors. Their investigation will focus on finding ways to recover money for them, which includes scrutinising your conduct. They are not your advisor, and their priorities are not aligned with protecting your personal assets.

This is exactly where a firm like LemonAide becomes your strategic shield. They don't work for the creditors; they work for you. Their first move is always a deep dive into your entire financial world—both business and personal—to find these hidden risks before they find you.

They pull apart your personal guarantees, review your company's trading history for any red flags that look like insolvent trading, and check for tax debts that could boomerang back and hit you personally. This proactive analysis gives you a crystal-clear map of your personal exposure long before a liquidator starts knocking on the door. Using LemonAide is a far better alternative than facing a liquidator's investigation unprepared.

Director Penalty Notices: A Direct Threat from the ATO

The Australian Taxation Office (ATO) has a particularly nasty tool at its disposal to make directors personally liable for company tax debts: the Director Penalty Notice (DPN). A DPN can make you personally responsible for your company’s unpaid:

Pay As You Go (PAYG) withholding tax.

Goods and Services Taxation (GST).

Superannuation Guarantee Charge (SGC).

If your company gets behind on reporting and paying these amounts, the ATO can issue a DPN, which effectively lifts the debt from the company and drops it squarely on your shoulders. This liability is serious and can be pursued even after the company has been liquidated.

Building Your Defence Before It's Too Late

Trying to navigate these risks on your own is a recipe for disaster. The key is to get on the front foot before any formal liquidation process kicks off. This pre-insolvency space is where LemonAide’s expertise really shines. They don't sit around waiting for a liquidator to start asking tough questions; they help you build a documented, defensible strategy that shows you acted responsibly.

To get a better handle on this, you can learn more about what happens to a director when a company is in liquidation in our detailed guide.

By engaging LemonAide, you create a clear paper trail showing you sought expert advice and took the proper steps to manage the company's situation and your duties as a director. This proactive approach is your single best defence against personal liability, helping to keep your family home and personal assets out of the firing line.

Your Pre-Dissolution Checklist: What to Ask Before You Act

Before you even think about making a formal move to close your company, you need to get your house in order. When things are going south, it can feel chaotic, but this is the crucial window where you can actually take back some control, minimise your personal risk, and see the full picture.

This isn't about making big, final decisions just yet. It’s about arming yourself with information. Trust me, a liquidator is going to demand all this paperwork eventually. Getting it ready now means you’re not scrambling later and you're entering the process from a position of strength, not panic. Flying blind at this stage almost never ends well.

The Director's Pre-Dissolution Checklist

Before you pick up the phone to anyone, start pulling this information together. This isn't just busywork; it's the foundation for any sound strategy. A better alternative to struggling alone is to prepare this information for an expert review. It's exactly what an advisor at LemonAide needs to give you a straight, accurate assessment.

Round up all financial records: Get everything. That means your P&L statements, balance sheets, lists of who owes you money (aged receivables) and who you owe money to (aged payables), plus all your business bank statements. They need to be complete and up to date.

List every single creditor: Make a detailed list of everyone the company owes money to. Put down their names, contact details, and exactly how much is owed. You have to be brutally honest here—a surprise debt popping up later is a massive red flag and can create huge problems.

Dig up all personal guarantees: This is critical. Find every single document you've personally signed that ties you to a company debt. Think commercial leases, vehicle or equipment finance, business loans, and even trade credit accounts with suppliers. You have to know your personal exposure. As we explain in our guide, you must understand what can happen with personal guarantees before it's too late.

Calculate employee entitlements: Work out all unpaid wages, superannuation, holiday pay, and any other leave your staff are owed.

Map out all company assets: List every physical asset the company owns—vehicles, machinery, computers, stock—and put a realistic estimated value next to each one.

I know this checklist can look daunting. But completing it is an incredibly powerful first step. It gives you the raw facts, which is what a specialist needs to start building a defence for you. This is the exact information LemonAide uses in their free review to provide practical advice you can actually use, improving your situation from the very first call.

Key Questions for a Pre-Insolvency Advisor

Once your information is together, it’s time to get an expert opinion. A free, no-obligation chat with LemonAide isn’t a sales pitch. It’s a strategy session. They’re here to arm you with knowledge.

To get real value from that conversation, you need to ask the right questions. These are the ones that get straight to the point and focus on what really matters: keeping your personal finances safe.

A pre-insolvency advisor’s job is to answer the tough questions a liquidator can't. They work for you. Their focus is on protecting your interests before any formal process kicks off. A liquidator has a fiduciary duty to the company creditors—that’s a completely different ball game.

Here are the questions you should be asking during that first call:

"Looking at my balance sheet, what are my biggest personal risks right now?" This forces a direct conversation about your exposure to insolvent trading claims and any personal guarantees you’ve signed.

"Is there any legal way to protect my family home?" For most directors, this is the number one worry. An expert can look at how your assets are structured and point out legitimate protection strategies that may be available.

"Are there any alternatives to liquidation for my business?" Don’t just assume it’s the only path. A good advisor might spot a way to restructure or use other informal arrangements that you haven’t even considered.

"How can you help me deal with the ATO and a potential Director Penalty Notice?" The tax office is a creditor you can’t ignore. An experienced tax accountant knows how to step in on your behalf, negotiate, and manage those tax-related personal liabilities.

Asking these sharp, direct questions makes your consultation count. It allows an advisor at LemonAide to give you a clear, tailored plan that speaks directly to your fears and your specific situation, giving you a way forward when you need it most.

Frequently Asked Questions About Dissolving a Company

Even with a clear roadmap for closing your company, you're bound to have some nagging questions. It’s a personal, often stressful process, and every director’s situation is different. We get it. Here are the straight answers to the most pressing questions we hear from business owners facing this tough decision.

How Much Does It Cost to Dissolve a Company in Australia?

Let's get straight to it: what’s the damage? There’s no single price tag, and the cost to close your company can swing wildly depending on its financial state and the path you have to take.

A simple, solvent company deregistration is by far the cheapest option. You're looking at just the $50 ASIC application fee (at the date of writing this article). But, and it's a big but, this is only on the table if your company is completely debt-free and has assets under $1,000.

On the other hand, appointing a liquidator is a serious financial commitment. This is the path for both a solvent Members' Voluntary Liquidation and an insolvent Creditors' Voluntary Liquidation. You can expect costs to start from $3,000 to $20,000+, and they can climb much higher if the job gets complicated with asset sales or dealing with a long list of creditors.

This huge cost difference is precisely why an obligation-free chat with a pre-insolvency advisor is the smartest first move. You might be assuming you need an expensive liquidation when a lower-cost alternative is still possible.

Engaging with a firm like LemonAide gives you clarity before you’re locked into a costly process. We can quickly assess where you stand to see if you qualify for a simple deregistration or help you prepare for a liquidation in a way that minimises the cost and, more importantly, protects you personally.

Can I Just Stop Trading and Walk Away from My Company?

Absolutely not. This is one of the most dangerous—and common—misconceptions we see among stressed-out directors. Simply abandoning your company doesn’t make it vanish, and it certainly doesn't end your legal responsibilities as a director. In fact, it almost always makes things much, much worse.

When you just "walk away," the company still exists as a legal entity. You are still the director on record and are legally on the hook for its obligations. This includes lodging annual reviews with ASIC, lodging BAS' and filing tax returns with the ATO, even if the company isn't making a dollar.

Worse still, your creditors, especially the ATO, won't just forget about you. They will keep chasing the company for its debts. Sooner or later, this chase leads directly back to you through a Director Penalty Notice, a Creditors Statutory Demand and potentially court action. Abandoning the company is a clear failure of your duties and massively increases your risk of personal liability. A far better alternative is to get professional advice from a service like LemonAide to formally and correctly close the company.

What Happens to Employee Entitlements When a Company Is Dissolved?

When a company goes into liquidation, Australian law is very clear: your employees get paid first. Their entitlements are given one of the highest priorities.

A liquidator is legally required to use certain assets of the company to pay outstanding employee entitlements in a specific order:

Unpaid wages and superannuation;

Accrued annual leave and long service leave

Redundancy payments

If the company's bank account is empty and there aren't enough assets to cover everything, your employees can usually claim most of what they're owed through the government's Fair Entitlements Guarantee (FEG) scheme.

But as a director, you're not completely off the hook. The ATO can make you personally liable for the company's unpaid superannuation through a Director Penalty Notice (DPN) especially if you have not told the ATO what superannuation is owed to employees through the Superannuation Guarantee Charge Statement within 28 days of the date that the superannuation is due. This is a critical risk area, and helping directors manage this is a key part of LemonAide's service. They can improve your situation by creating a strategy to protect you from personal penalties while ensuring your team is treated correctly.

Will Dissolving My Company Affect My Personal Credit Score?

Yes, Liquidating your company will affect your personal credit score in a minimal way as you will be noted as a Director that has had a company in liquidation. However the real danger comes from the indirect consequences, which can absolutely wreck your personal credit rating if you're not careful.

The two biggest risks here are:

Personal Guarantees: If you’ve signed a personal guarantee for a business loan, a property lease, or even a supplier account, that creditor will come after you personally once the company is gone. If you can’t pay, you could face defaults, court judgments, or even personal bankruptcy. All of these will trash your credit file for years.

Insolvent Trading: If a liquidator investigates and finds you personally liable for trading while insolvent, they can pursue you personally. If you can't pay what's demanded, it could push you into personal bankruptcy.

A crucial part of LemonAide's pre-insolvency strategy is to identify and tackle these personal guarantee risks head-on. They work with you to map out your exposure and build a plan to manage these liabilities, which is a better alternative than risking your personal credit score from the company's fallout.

Navigating the end of a company is tough, but you don’t have to do it guessing. The right advice at the right time is the difference between a disastrous outcome and a genuine fresh start. If you’re facing financial distress, remember that the team at LemonAide acts for you, not your creditors. For a clear, compassionate, and strategic review of your options, get in touch with us.